Probably everyone knows about the need to use cash register equipment (CCT) when making cash payments. We are all buyers of goods and consumers of services, and it is the cash receipt that serves as confirmation of the fact of payment for the goods, work or service. If something happens, it is the cash receipt that allows us to defend our consumer rights and receive after-sale or warranty service.

But let's look at the cash register from the point of view of the business owner; he is hardly happy about the need to use cash registers, so let's figure it out - is it possible to do without cash register equipment when accepting cash? And if you still need a cash register, then understand how to choose it and register it?

In what cases is a cash register used?

The need to mandatory use a cash register on the territory of the Russian Federation by all organizations and individual entrepreneurs when making cash payments or using them is established by Article 2 of the Federal Law of May 22, 2003 No. 54-FZ “On the use of cash registers.”

At the same time, you can often observe how trade or provision of services is carried out without a cash register. Are all these entrepreneurs breaking the law? No, they do not violate, but simply know about their right not to use a cash register in some cases when paying in cash or with a payment card. And there are several such possibilities.

- Until July 1, 2018, payers (organizations and individual entrepreneurs), as well as individual entrepreneurs working for , have the right to accept payment in cash without using a cash register (Article 2.1 of Law No. 54-FZ). If the buyer or client requires a document to confirm the fact of payment, then a sales receipt or receipt must be issued instead of a cash receipt.

- Until July 1, 2019, organizations and individual entrepreneurs may not use a cash register, regardless of the taxation regime, if they provide services to the population (Article 2 of Law No. 54-FZ). In this case, it is mandatory, and not at the request of the client, to issue. The procedure for registration and issuance of BSO is given in the Decree of the Government of the Russian Federation of May 6, 2008 N 359. Examples of strict reporting forms include transport tickets, receipts, movie tickets, subscriptions, work orders, coupons, tourist and excursion vouchers, etc.

- Organizations and individual entrepreneurs, due to the specifics of their activities or location, can make payments in cash or payment cards without using a cash register when carrying out the following types of activities:

- sales of newspapers, magazines and related products in special kiosks, while the share of the sale of newspapers and magazines in their turnover must be at least 50 percent, and the range of related products must be approved by the local government;

- sales of travel tickets and coupons for travel on city public transport;

- sales of securities and lottery tickets;

- providing meals to students and employees of educational organizations implementing basic general education programs (that is, in kindergartens and schools);

- selling ice cream and soft drinks on tap at kiosks;

- trade from tanks in beer, kvass, milk, vegetable oil, live fish, kerosene, waddling vegetables and melons;

- peddling small retail trade in food and non-food products;

- organizations and individual entrepreneurs located in remote or hard-to-reach areas (with the exception of cities, regional centers, urban-type settlements) specified in the list approved by the local government, etc.

For a complete list of such activities, see Article 3 of Law No. 54-FZ.

Please note: from 31 March 2017, all retailers of alcohol, including beer, must use a cash register. The requirement also applies to those selling beer in public catering.

What should payers and individual entrepreneurs working for pay attention to? Retail trade in these modes does not include the sale of food and beverages in public catering establishments. There are known court cases where organizations on UTII selling food and drinks in catering establishments were fined 30,000 rubles for trading without issuing documents confirming payment, because they believed that they had the right not to use a cash register, as imputed tax payers. The law equates sales in public catering establishments to services to the public, therefore each client (buyer) must be issued a BSO or cash receipt.

What should a cash register be like?

From February 1, 2017, registration of old-style cash registers that do not have Internet connection functions will cease. Until July 1, 2017, all sellers already working with cash register systems must upgrade their equipment, if possible, and re-register with the tax office. If the existing cash register does not allow modernization, then you need to purchase a new one and register it. The requirements for a cash register are given in Article 4 of the Law of May 22, 2003 N 54-FZ “On Cash Register Machines”.

Cash register equipment must:

- have a case with a serial number;

- there must be a real time clock inside the case;

- have a device for printing fiscal documents (internal or external);

- provide the ability to install a fiscal drive inside the case;

- transfer data to a fiscal drive installed inside the case;

- ensure the formation of fiscal documents in electronic form and their transfer to the operator immediately after entering the data into the fiscal drive;

- ensure printing of fiscal documents with a two-dimensional bar code (QR code no less than 20 x 20 mm in size);

- receive confirmation from the operator of receipt of data or information about the absence of such confirmation;

- provide the ability to read fiscal data recorded and stored in memory for five years from the end of operation.

We also draw your attention to the fact that the so-called check printing machines (CHMs) are not recognized as a cash register for registration with the tax office. Only payers of UTII and PSN can use such devices in order to issue the buyer a document confirming the receipt of funds for the purchased goods.

You can purchase new cash registers only from the cash register register published on the official website of the Federal Tax Service. The cost of a new cash register with an Internet connection averages from 25 to 45 thousand rubles, tariffs for the services of fiscal data operators - from 3,000 rubles per year.

Since 2017, fines for not using cash registers for cash payments, using a cash register that does not meet the requirements established by law, as well as for violating the conditions for registration and use of cash register equipment are (Article 14.5 of the Administrative Code of the Russian Federation):

Failure to use a cash register if it should be used:

- from ¼ to ½ of the purchase amount, but not less than 10,000 rubles for individual entrepreneurs and heads of organizations;

- from ¾ to the full purchase amount, but not less than 30,000 rubles for legal entities;

Use of old cash registers or violation of the procedure for their registration/re-registration:

- warning or fine from 1,500 to 3,000 rubles for individual entrepreneurs and heads of organizations;

- warning or fine from 5,000 to 10,000 rubles for legal entities.

Refusal to issue a paper or electronic check to the buyer:

- warning or fine of 2,000 rubles for individual entrepreneurs and heads of organizations;

- warning or fine of 10,000 rubles for legal entities.

Registering a cash register

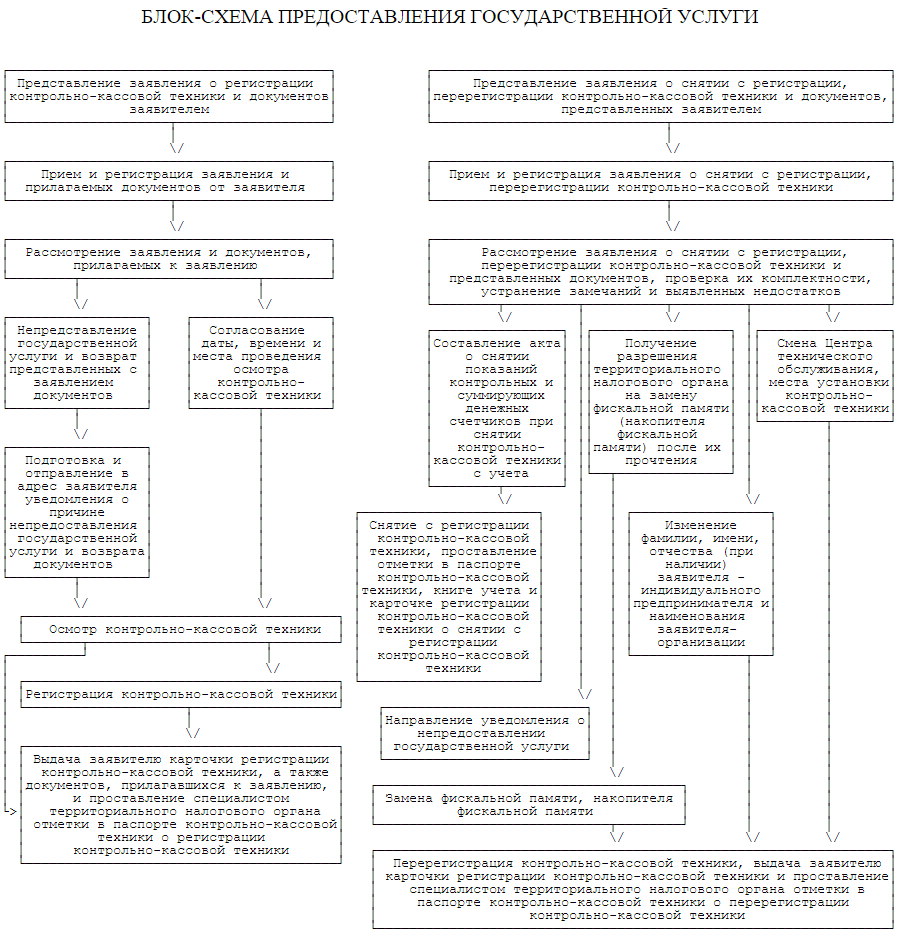

Registration of cash registers is regulated by special Administrative Regulations, approved by Order of the Ministry of Finance dated June 29, 2012 No. 94n. Appendix No. 2 to this regulation provides a flowchart for the provision of public services for registration, re-registration and deregistration of a cash register. The block diagram below can be enlarged by clicking on it.

Individual entrepreneurs register a cash register with the tax office at their place of registration, and organizations - at their legal address. If the cash register is not located at the legal address of the organization, then you will have to create a separate division at the place of trade or provision of services, and the cash register registration will take place at this address.

In cases where an organization has several separate divisions (for example, stores), subordinate to different tax inspectorates, but located in the same municipality, all cash registers can be registered with one tax office at the taxpayer’s choice.

Documents for registration of cash registers are submitted according to the list given in Article 25 of the Administrative Regulations:

b) passport of cash register equipment;

c) a technical support agreement concluded with the supplier or technical service center (TSC), an authorized supplier to provide technical support for the registered model of cash register equipment.

This list is exhaustive, but in practice the tax office may additionally request a number of documents, for example, such as:

- a lease agreement for the premises where the cash register will be located, or a certificate of registration of the right to the premises, if it is owned;

- journal of the cashier-operator according to the KM-4 form;

- logbook for calling technical specialists in the KM-8 form;

- documents confirming the fact of purchase of the cash register.

These requirements can be disputed, but you can also take these documents with you. And, of course, if the cash register is not registered personally by an individual entrepreneur or the head of an organization, then a power of attorney will be required to carry out registration actions. After accepting the documents, the tax inspector agrees on the date, time and place of inspection of the cash register, and if it is bulky, then it is quite possible to go to the location of the cash register.

The inspection and verification of the cash register is carried out by a tax inspector in the presence of a representative of the taxpayer (individual entrepreneur, head of the organization or authorized representative) and a specialist from the central service center. The tax inspector checks the taxpayer's data, which the service center employee enters into the cash register. The cash receipt must contain mandatory details, such as the full name of the individual entrepreneur (name of the organization), TIN, serial number of the device, date, time and cost of purchase, serial number of the receipt.

Next, the cash register is fiscalized, that is, it is transferred to the fiscal mode of operation. The tax inspector enters a special digital code that protects the fiscal memory from hacking, after which the central service specialist installs a seal on the cash register. The tax inspector must make sure that the cash register is in good working order, then registers the device in the accounting book, makes notes in the passport and academic certificate, certifies the cashier-operator’s log and issues a cash register registration card. The cash register is ready for use and can be used.

In what cases may it be necessary to re-register a cash register? These grounds are given in paragraph 75 of the Administrative Regulations:

- replacement of fiscal memory or fiscal memory storage device (EFS);

- changing the address of the location where the cash register is installed;

- changes in the full name of an individual entrepreneur or the name of an organization;

- CTO changes.

To re-register a cash register, you must contact the tax office where the cash register is registered, with an application in the form approved by Order of the Federal Tax Service of Russia dated 04/09/2008 No. MM-3-2/152@, a cash register passport and its registration card. When replacing EKLZ, you must also attach to these documents the conclusion of the Central Technical Service (if available).

Re-registration of a cash register is carried out during a personal inspection of the device by a tax inspector for serviceability, integrity of the case, presence of seals and the “Service” sign. Just as during the initial registration, the presence of a specialist from the central service center and the taxpayer is required. Re-registration notes are included in the passport and cash register registration card.

More details:

Action plan for registering a cash register

- Select a cash register from the models listed in the state register.

- Contact the general supplier or the central service center to purchase the CCP.

- Submit documents for registration to the tax office at the place of residence of the individual entrepreneur, at the legal address of the organization or the address of a separate division (if the cash register is not located at the legal address of the LLC).

- Ensure inspection and fiscalization of the registered cash register by a tax inspector in the presence of a central service center specialist.

- Do not forget about the need to re-register CCP when replacing EKLZ and other grounds established by law.

An innovation next year for many business entities in carrying out their activities will be the mandatory use of online cash registers. What are online cash registers and who will use them? Let’s look at them in more detail here. By these we mean cash registers, which will transmit all information from these machines to the tax office in real time through the OFD.

It was possible to switch to new equipment on a voluntary basis back in 2016. But from the beginning of February 2017, it is no longer possible to re-register or register the old cash register.

Also, you cannot continue working simply by changing the ECLZ. In this regard, entrepreneurs and companies whose deadline for re-registering their existing devices has come up are required to deregister them and purchase a new online cash register.

At the moment, taxpayers who are in the general or simplified regime are required to use the new type of devices - that is, those who need to take into account the income received to calculate the tax.

All those who have currently been exempted from recording revenue on the cash register - those who use UTII or who have purchased a patent - must begin to use it from July 2018 without fail.

Attention! Also, from March 31, 2017, sales of beer and alcoholic beverages were introduced, regardless of the taxation system. This means that if UTII is applied and alcoholic beverages are sold, the cash register must be used. At the same time, the new device must also be able to work with the EGAIS system.

In what cases can you not use online cash registers?

The use of online cash registers is mandatory, but in some cases they may not be carried out, but this list is strictly limited and cannot be arbitrarily expanded. Several factors will be taken into account - from the lack of ability to connect to the Internet to a subjective assessment of trade relations.

These cash registers may not apply the following categories:

- Church organizations.

- Credit organizations that use ATMs in their work.

- Sellers of magazines and newspapers.

- Porters at airports and train stations.

- Persons who carry out peddling trade.

- Entities engaged in trade in ice cream and bottled soft drinks.

- Drivers and conductors who sell travel tickets.

- Sellers at retail fairs and markets.

- Issuers of securities.

In addition, CCT may not be used by individual entrepreneurs who provide care and supervision to the sick and children, who repair shoes, as well as rent out real estate.

Pharmacies and stores located in hard-to-reach places and remote areas can also receive this preference. If they issue payment documents to customers, then they have the right not to use new cash registers. This is due to the lack of Internet in such places. But stores located in urban settlements and regional centers will use new equipment on a general basis.

If stores are located in areas where the Internet is completely absent, they will carry out their activities using conventional cash register equipment.

Is it possible for an exempt person not to use a cash register?

Entrepreneurs and firms that did not use cash registers when the new law came into effect may continue not to use them until July 1, 2018. From this day on, they will need to be used without fail, even if subjects were previously exempted from this.

Thus, online cash registers will only be relevant in two years. Likewise, there is no need to purchase online cash registers for, as well as for those who, instead of punching cash receipts, issue BSO.

Expenses for upgrading cash register equipment can be used as a tax deduction, but not more than 18,000 rubles for each device.

Cost of online ticket offices and services

From July 1, 2017, it will be possible to use only those cash registers that can transmit information about punched checks. But this does not mean that you will have to buy a new online cash register for this. Some models will simply need to be improved by installing a fiscal drive and special software. Unfortunately, the cost of a complete replacement is currently difficult to estimate, but manufacturers of cash registers assure that online machines will be comparable in price to the old ones.

However, the benefits for organizations when using new types of devices will be obvious. Firstly, there will no longer be a mandatory need to enter into an agreement with a service company. In addition, the procedure for registering a cash register with the tax office will be simplified.

At the same time, you will need to conclude an agreement with the OFZ operator, who will act as an intermediary between the company and the tax office. Approximately, the cost of such services will be about 3,000 rubles per year. The outlet will also need to provide an Internet connection.

The average price for servicing a cash register is now 6,000 rubles per year. Thus, savings from switching to an online cash register from 2017 will amount to up to 3,000 rubles annually.

What do you need to register an online cash register?

Before you begin the procedure for registering a new cash register, you must, of course, select and purchase the device itself. There is a register of cash registers approved for use, which can be viewed on the Federal Tax Service website.

Before you begin the procedure for registering a new cash register, you must, of course, select and purchase the device itself. There is a register of cash registers approved for use, which can be viewed on the Federal Tax Service website.

When choosing a cash register for work, it is necessary, first of all, to take into account the planned range of goods, as well as the number of transactions per day. It is also worth highlighting special cash registers for online stores that do not print out a paper receipt, but at the same time always send its electronic version to the client’s email.

According to the law, the new technology has the function of transmitting information about each check via the Internet to the tax office. Therefore, you need to immediately choose how exactly the connection will be made - through a SIM card of a cellular operator, through a wired or wireless Internet connection.

Attention! Most tax services insist that registration of new cash registers be carried out only electronically using the “Taxpayer Personal Account”. In order to use it, an organization or entrepreneur must have a qualified digital signature. It can be obtained from one of the operators with the appropriate license. It usually takes several days to issue a digital signature.

The computer from which registration will be carried out must have a special encryption program “Crypto-Pro” installed. A license for its use can usually be purchased from the same company where the EDS was ordered.

Access to the tax website should only be done using Internet Explorer version 7 or higher. However, it is recommended to immediately update it to the latest available one.

How to register an online cash register - step-by-step instructions

The tax office requires that the cash register be registered only using a personal account. This can be done independently, or for an additional fee at the dealer or at a device servicing center.

Registration on the website of the fiscal data operator

Before starting the cash register registration procedure, you need to select an intermediary who will store information about punched checks and transfer them to the tax service. Moreover, such a company must have appropriate accreditation - permission from the tax authorities to carry out all of these operations. A register of such organizations is available on the tax website, which anyone can view. As of April 2017, it included five companies.

Registration with each of these operators is no different in nature. However, your personal account can provide various options for viewing and processing punched checks. If this is possible, then before registering, it is best to try each of the operators in demo mode and then choose the one that will be more convenient than the others.

During registration, you will need to indicate the company name, legal address, TIN and OGRN codes, and contact information. Sometimes registration needs to be confirmed with an electronic signature, which must also be qualified.

Conclusion of an agreement with OFD

After registering in your personal account, you need to draw up an agreement with the OFD. To do this, you need to click on the button or select the “Conclude an agreement” menu.

Primary information will be obtained from the electronic signature - company name, INN and OGRN. The rest will need to be entered manually. These include, in particular, a document that gives authority to the manager, legal and actual addresses. It is important to indicate the address correctly, since all necessary documents will be sent to it in paper form - invoices, certificates of completed work, etc.

After drawing up, the contract is usually sent for approval to the OFD employees, and after their approval it can be signed. This action can be performed using a qualified digital signature.

Get access to your OFD personal account

After the agreement between the user and the OFD is signed, you can fully use your personal account. Currently, it does not contain any information - it will begin to accumulate only after registration and connection of the first cash register.

Typically, using your personal account you can obtain the following information:

- Checks punched at the cash register, from the contents (in quantitative and total terms). The receipt can usually not only be viewed, but also downloaded electronically;

- Reports confirming the opening and closing of shifts;

- List of cash registers connected to this OFD;

- Reports of various contents - on broken checks, the average price of a check, the average number of checks over a period of time, etc.;

- Employees who have access to personal account information. It is possible to indicate which functions a particular employee has the right to use;

- Exchange of documents between the user and OFD - agreements, acts, invoices, etc.

The functions that can be used in your personal account may be different for different OFDs.

Registration on the website tax ru.

Registration of an online cash register with the Federal Tax Service is carried out mainly through a personal account on the tax portal. To access it, you need to use a qualified one.

If the personal account on the nalog.ru portal is not open to the taxpayer, you must first carry out the opening procedure. Access is provided via a direct link from the Federal Tax Service website. It should be taken into account that the personal account for a legal entity and an entrepreneur have differences.

If the personal account on the nalog.ru portal is not open to the taxpayer, you must first carry out the opening procedure. Access is provided via a direct link from the Federal Tax Service website. It should be taken into account that the personal account for a legal entity and an entrepreneur have differences.

As soon as you log into your personal account, you should click on the “Cash register equipment” tab, and then the button with “Register cash register equipment” on it.

After this, a window will appear into which the data is entered sequentially:

- The address where the online cash register will be installed for use - it must be complete.

- Names of place of use. It is selected in any form. You can name, for example, store No. 1, etc.

- The model of the online cash register, as well as its serial number. The brand of the device is selected from the drop-down list. If there is no CKA model in it, this means that the search in the list is carried out incorrectly or that the device owned by the company is not authorized for use.

- The model of the fiscal drive and its number.

- It is necessary to note, if necessary, a special mode of using an online cash register (online store, delivery or peddling trade). When the normal mode of operation of the cash register is assumed, there is no need to install anything here.

- The name of the FD operator - it must also be selected from the drop-down list of registered accredited operators. The OFD TIN will be automatically filled in.

Next, you need to check all the entered information and if everything is correct, click on “Sign and send”. To this request, the Federal Tax Service must send a response, which, if registration is successful, will contain the number assigned to the online cash register. This details will need to be used in the future when registering a cash register with the OFD.

Attention! The KKA number received from the tax office must be entered into the machine. After this, a special receipt will be printed at the online checkout, in which it will be indicated. Next, in your personal account, you need to click on “Complete registration” and in the window that appears from the printed check, enter the relevant data: date and time, fiscal document number (FD line) and fiscal attribute (FN line). After this, the cash register will be ready for use.

We register the cash register with the OFD

Setting up an online cash register with an FD operator is carried out on its website. A representative of a company or individual entrepreneur needs to log into his personal account. Next, use the “Add cash register” or “Register device” buttons. This action can be performed only after the online cash register has been registered in the taxpayer’s personal account and the Federal Tax Service Inspectorate has assigned a number to the cash register.

In the pop-up window you need to fill in the following information:

- KKA number, which was assigned to him by the tax office when registering him.

- Online cash register number assigned to it by the manufacturer. It can be viewed in the device passport.

- Online cash register model, it is also indicated in the passport.

- The number that is located on the fiscal drive. It must be recorded in the cash register passport.

The FD operator may also offer additional services. This includes, in particular, reminders about the approaching expiration date of the fiscal drive, or that the cash register has not been used for a long time.

In the system, each online cash register can be called by some short and convenient name, so that it can be easily identified and reports on its operation can be compiled. It is proposed for enterprises with several retail locations to assign names to devices based on location. It may coincide with the name of a store, street, locality, etc.

After registering the cash register in the system, you need to create an invoice to pay for the operator’s services, according to the selected tariff. It is generated automatically.

Attention! The cash register will be activated after the bill has been paid in full, only then will the online cash register be able to transmit information and checks will be processed on it.

As soon as the paid period ends, the business entity will again need to repeat the entire procedure for generating an invoice for payment.

Is it necessary to keep a cashier-operator log for online cash registers?

The use of old-style cash registers required the need to fill out a special journal for the cashier-operator, which was issued for each cash register and recorded the cash revenue generated on this machine for each day or shift. A separate form was approved for it.

Attention! In September 2016, the Federal Tax Service issued an explanatory letter in which it acknowledged that keeping a cashier-operator journal is no longer mandatory. This is due to the fact that all the necessary data on transactions performed at the online cash register are transferred to the FD operator’s server.

However, if a business entity has such a need, then for internal purposes it can continue maintaining the cashier-operator journal.

The new legislation provides for a number of mandatory documents that must be completed when using online cash registers. Such forms include reports on the status of settlements, on the opening or closing of a shift.

According to new legal requirements, in Russia businessmen and entrepreneurs must have cash register equipment registered with the tax service.

We will tell you in detail how to register cash register equipment on the tax authorities’ website.

Cash register equipment must comply with the requirements and standards of current legislation. The cash register must connect to the Internet, have modern software and be multifunctional and universal.

The Meta technical service center employs highly qualified specialists who will help you choose high-quality equipment for your type of business.

Stage 2. Modernization of the cash register

You can also modify your existing cash register model without buying a new one.

If you have not yet decided which option to choose, we recommend that you familiarize yourself with it. It will help you decide whether your cash register can be upgraded.

If you have any doubts, call the consultants of the Meta Center.

Stage 3. Registration and paperwork with the Federal Tax Service

Please note that the registration procedure applies not only to the new online cash register, but also to the updated old one. The modernization will still have to be confirmed.

The registration procedure can take place in different ways:

- Personal appeal to the tax service. You will need to prepare a written application and documentation package before going to the inspection.

- Registration of equipment through the Federal Tax Service website. You will need to register on the official website of the tax service and conduct transactions through your personal account. Remember, you must have received an ECES (enhanced qualification electronic signature), otherwise you will not be able to use this method.

- . Usually this service is paid.

- Registration of documentation through technical service centers. With this option, you will not need to deal with documents, since specialists will independently collect the necessary papers and send them to the Federal Tax Service. All you need is your consent to perform this service.

Each transaction in which money was spent or received must be formalized as required by law, both for cash and non-cash payments.

If the payment is made by non-cash method, then the bank monitors compliance with the rules for working with funds. However, the vast majority of small businesses prefer cash payments; for this it is necessary to maintain cash accounting documents:

Cash book;

Cashier-operator's journal;

Cash report.

Organizing cash accounting correctly is quite simple. To do this, you just need to timely reflect the receipt and expenditure of cash in the accounting books. It should be remembered that you can only accept money from customers using a cash register, and in some cases, using strict reporting forms.

The cash register should be used for cash payments, both with citizens and with organizations and individual entrepreneurs, only after you register it with the tax office. To do this, you need to: conclude an agreement for the maintenance of a cash register (CMC) with a technical service center (TSC), carry out fiscalization of the cash register, purchase visual control equipment, etc.

The legislation of the Russian Federation allows organizations to use only certain models of cash registers, that is, those that are included in the state register. It lists all models that are allowed to be used. In addition to the register, there is also a cash register classifier, which provides which cash register models are intended for each field of activity.

Organizations selling cash registers are divided into two categories:

1) specialized sales firms;

2) technical service centers.

You can only purchase cash registers from specialized sellers, but after that you will still have to enter into an agreement with the central service center for maintenance.

It is more convenient to buy the device directly at the service center. This organization sells, services, and repairs cash register machines.

You can also buy a used cash register. Advertisements for the sale of used cash registers are given by companies that have ceased operations and are now selling off their property. You can only buy devices that the seller has deregistered with the tax office. As confirmation, he must give you a KKM registration card with a mark from the tax office stating that the device has been deregistered.

Both new and used cash registers must be accompanied by a version certificate, technical data sheet and visual control means (VIC). These are round holographic stickers. It is allowed to use a cash register that has:

1) ICS “State Register”;

2) ICS “Service”.

ICS “State Register” indicates that the model corresponds to the reference sample. ICS “Service Maintenance” indicates that the cash register machine is undergoing maintenance. This hologram indicates the year when the machine was put into operation and put into maintenance.

Penalties for using a cash register without visual control are not provided for by the legislation of the Russian Federation. Responsibility can only arise for non-use of the cash register.

Before registering a cash register, ask the tax office whether you need to purchase visual control equipment or not. Decree of the Government of the Russian Federation dated July 30, 1993 No. 745 established the requirement to equip cash registers with internal control systems.

Moscow and St. Petersburg have additional requirements. Thus, it is necessary to use additional self-adhesive seals purchased at the service center. Before registering cash registers, the tax authorities of these cities must check the presence of such seals. The seal consists of a main part and a tear-off control coupon (an identification number is provided everywhere). On the main part, the service center specialist indicates the date of installation of the seal and signs it. This part is pasted on the cash register.

To obtain a seal, you must submit an application to the service center and pay the cost of the service. The seal will be issued no later than 15 days from the date of payment. The seal is valid for one quarter.

Documents needed when purchasing a cash register:

After you have purchased a cash register and entered into an agreement with the central service center for maintenance, the cash register must be registered with the tax authority.

The cash register must be registered with the tax authority at the place of registration.

The following must be submitted to the tax office:

Application for registration of cash register;

Completed cash register registration card in two copies;

Power of attorney for the right to register a cash register (if the cash register is not registered by the head of the organization);

KKM technical passport (original and copy);

KKM version passport (original and copy);

Contract for maintenance of cash register machines at the central service center (original and copy);

Visual control tools (holograms);

The cashier-operator's journal in form No. KM-4 - it must have numbered pages, laced, certified with the seal of the organization, as well as the signatures of the director and chief accountant or individual entrepreneur;

Registration card with a tax office mark on deregistration (for used devices).

Tax authorities may also require other documents: originals and copies of the certificate of state registration of a legal entity and certificate of registration with the tax authority. In addition, you may also have to submit a copy of the lease agreement for the premises where the cash register will be installed.

From the moment the documents are received, the tax authorities are required to register the cash register within five days, and within the same period, a representative of the tax authority must check the machine.

Participating in the registration procedure are:

Employee of the KKM registration department of the tax inspectorate,

Technical service center specialist,

Representative of the organization.

As a rule, the tax authority sets certain days for submitting and receiving documents and fiscalizing the apparatus. First, the new cash register is fiscalized, because the cash register is purchased in a non-working (non-fiscal) mode, i.e. the counter that summarizes the daily revenue is not yet turned on. If you bought a used cash register, you will also have to go through the fiscalization procedure.

Fiscalization is as follows. The central service specialist enters its serial number into the cash register’s memory, programs the name of the owner company and its tax identification number. The tax inspector then sets a digital password that protects the fiscal memory from hacking. This password is known only to the tax officer. Then the service center specialist seals the car, putting his seal. The date of sealing and information about the stamp imprint are recorded in the journal of form No. KM-8. After this, in the KKM technical passport in the “Commissioning” section, the central service specialist signs and indicates his certificate number.

Next, testing of the cash register begins. The notional amount is entered and the correctness of the details on the check is checked. The tax inspector enters a secret password and takes a trial report from the fiscal memory.

Upon completion of fiscalization, the tax inspector assigns a number to the cash register and makes an entry in the organization’s cash register book, which is maintained by the tax authorities. The tax inspector endorses the cashier-operator's journal (form No. KM-4), puts the tax office stamp on it and records the date of fiscalization. Then the tax inspector fills out the KKM registration card and endorses it from the head of the tax authority. This card must be located where the cash register is installed.

The registration card indicates the address where the cash register will be installed. If an entrepreneur has several stores (cafes, workshops, etc.), then it may be necessary to move the cash register to another location. This can only be done by first notifying the tax authority. The tax inspector will make an entry in his journal and make changes to the registration card. Otherwise, the organization will be held accountable.

If you have purchased a backup device that you plan to use while your cash registers are being repaired, you must notify the tax inspector about this in advance, who will make a corresponding entry on the registration card. This will allow the use of a backup device in any store (or any other location) owned by the organization.

To reduce taxes on the amount paid for cash registers, an important criterion is the type of activity of the organization. If the cash register is used only in activities subject to VAT, then the small enterprise has the right to deduct the entire tax. In this case, all standard conditions must be met: the device is put into operation, an invoice is received, where the tax amount is entered on a separate line - only in this case the “input” VAT can be deducted.

If a store sells both retail and wholesale, and retail trade is transferred to the payment of tax on imputed income, then cash registers are used both in activities subject to and not subject to VAT.

In this case, “input” VAT cannot be deducted. The “input” tax must be distributed in proportion to the cost of goods sold. That part of the tax that falls on goods whose sales are subject to VAT can be deducted. The remainder of the tax amount is included in the initial cost of the cash register. When calculating this proportion, they take the cost of goods sold for the tax period in which the cash register was put into operation.

Example 2.13. In April 2008, the LLC bought a cash register for its store for 17,700 rubles. (including VAT - 2700 rubles). Commissioning costs, consisting of fees for visual inspection equipment and programming, are equal to RUB 1,310. (including VAT - 200 rubles). The company's revenue this month amounted to 890,000 rubles: - 471,000 rubles. (including VAT - 71,848 rubles) - from wholesale sales (general taxation system); - 419,000 rubles. – from retail sales using cash register registers (UTII). The amount of “input” VAT that the LLC must include in the initial cost of the cash register will be 1,479 rubles. [(2700 rubles + 200 rubles) x 419,000 rubles: (890,000 rubles – 71,848 rubles)]. The remaining tax is 1,421 rubles. [(2900–1479)] - can be deducted after the cash register is put into operation. The LLC has established the same service life of the cash register in accounting and tax accounting - 6 years (72 months). It was decided to calculate depreciation in accounting and tax accounting using the straight-line method. The initial cost of the cash register is 17,589 rubles. [(17,700 rubles – 2700 rubles + 1310 rubles – 200 rubles + 1479 rubles)], i.e. the amount of monthly depreciation will be 244.29 rubles. .

Before handing over the cash register for repairs, the enterprise must take readings from the control cash meters and enter the received data into the report in form No. KM-2. This must be done because during repairs these counters may reset to zero. For the same reason, before the start of repair work and after its completion, the act must be endorsed by a tax inspector.

But in practice, most tax inspectorates do not require a report to be submitted to them before starting repairs, unless the malfunction is related to the fiscal memory unit or other devices that can cause control cash counters to be reset. The central service technician must check the condition of the fiscal memory unit and write down his conclusion in the report before starting the repair. Since cash registers last more than one year, they are taken into account as part of fixed assets, their cost is reflected in account 01 “Fixed Assets”.

In order to sell a cash register, it is necessary to deregister the cash register with the tax authority. An application requesting this is drawn up in any form. The following documents must be attached to the application:

KKM registration card;

Journal of the cashier-operator.

When deregistering a cash register, the organization must confirm that the readings of the summing cash counters are fully reflected in the cashier-operator's journal. To do this, attach the final check, punched on the same day when the application to deregister the cash register was submitted to the tax office. It is understood that, having entered the final receipt, the company no longer uses this cash register.

If a tax inspector wants to check the condition of the fiscal memory block. In this case, he goes to the enterprise (or the cash register is brought to the tax office) and takes readings from control cash counters. The data obtained must correspond to the entries in the cashier-operator's journal.

In a number of cases, before deregistering a cash register, tax inspectorates require the enterprise to set the readings of the summing cash counters to zero. This operation is carried out and documented in an act according to form No. KM-1 by a specialist from the Central Technical Service. The act must be signed by a tax inspector.

After checking the readings of the cash counters, the tax inspector gives the enterprise a cashier-operator book and a copy of the registration card with a note about the deregistration of the cash register.

If it was not possible to sell the KKM, and they decided to simply write it off, then you need to draw up an act for writing off the fixed asset. The act must indicate the reason why the cash register is retired (physical or moral wear and tear). The characteristics of the vehicle being written off are also given here: its make, service life, inventory and serial numbers, as well as the original and residual value. The act is drawn up after the cash register is deregistered with the tax authority.

You can work without a cash register when trading:

Newspapers and magazines;

Lottery tickets;

Tickets and coupons for travel on public transport;

Ice cream;

Non-alcoholic drinks on tap;

From tanks with beer, kvass, milk, vegetable oil, live fish, kerosene;

Waddled with vegetables and melons;

Food and non-food products from hand carts, baskets, trays;

Food products from open stalls in covered markets.

Entrepreneurs and organizations providing household services to the population can also pay in cash without a cash register. They are allowed to use strict reporting forms instead of a cash register.

It is impossible to accept money from organizations without a cash register, therefore, if clients include both individuals and legal entities, a cash register is necessary.

In a one-time transaction, it is more profitable for an individual entrepreneur not to buy a cash register, but to pay a fine. Responsibility for failure to use a cash register is provided for in Art. 14.5 of the Code of the Russian Federation on Administrative Offenses (CAO RF). The amount of the fine that can be collected from an official of an organization is from 3 thousand to 4 thousand rubles, from a legal entity - from 30 thousand to 40 thousand rubles.

The purchase of a cash register, as well as the costs of its registration and maintenance, will require more money. Moreover, the entrepreneur may not have to pay a fine, since inspectors have the right to prosecute only if no more than two months have passed since the entrepreneur violated the procedure for handling cash. This is stated in paragraph 1 of Art. 4.5 Code of Administrative Offenses of the Russian Federation.

Before starting work at the cash register, the cashier receives from the manager the keys to the cash register, the keys to the drive of the cash register and cash drawer, loose change and banknotes in the amount necessary for settlements with customers. The cashier signs the book of accepted and issued money.

The manager is obliged:

In the presence of the cashier, take readings from sectional and control counters and compare them with the readings recorded in the cashier-operator’s journal for the previous day;

Make sure that the readings match, enter them in the journal for the current day at the start of work and certify them with your signature and the signature of the cashier;

Draw up the beginning of the control tape, indicating on it the type and serial number of the machine, the date and time of start of work, the readings of sectional and control counters, certify the data on the control tape with signatures (yours and the cashier’s) and close the lock of the cash counters;

Conduct training for cashiers and salespeople in accordance with the Standard Operating Rules for Cash Register Machines.

If malfunctions occur in the operation of the cash register, the cashier is obliged to:

Turn off the cash register, call the manager, determine the nature of the malfunction;

In case of unclear reflection of the details on the check, non-issue of the check or breakage of the control tape, together with the manager, check the prints of the check on the control tape, sign the check, indicating the correct amount on the back, and after checking the absence of numbering gaps, sign the places where the control tape is broken. If the check does not come out, then you should receive a zero check instead;

If it is impossible to continue work due to a malfunction of the cash register, the cashier, together with the manager, formalizes the end of work on this cash register, as at the end of a shift, with a note in the cashier-operator's journal for this cash register about the time and reason for the end of work.

If it is impossible to eliminate the malfunction on your own, then a specialist from the service center is called.

The cashier is prohibited from working without the control tape or gluing it in places where it is broken.

At the end of the working day or upon the arrival of the cash collector, the cashier must:

Prepare cash receipts and other payment documents;

Prepare a cash report.

After this, the manager, in the presence of the cashier, takes meter readings, receives a printout or removes the control tape used during the day from the cash register, signs the end of the control tape (printout), indicates on it the type and number of the machine, meter readings, daily revenue, date and time of completion of work . Indications at the end of the reporting day are entered into the cashier-operator's journal.

Based on the meter readings at the beginning and end of the day, the amount of daily revenue is determined. It must correspond to the readings of cash totaling counters and control tape.

The following details must be reflected on the cash receipt or insert document:

Name of the organization;

TIN of the organization;

Serial number of the cash register;

Serial number of the check;

Date and time of purchase;

Purchase cost;

Sign of a fiscal regime.

Checks are cleared simultaneously with the issuance of goods using stamps or by tearing in designated places. All checks punched on the cash register during the shift and not issued to customers (readings taken at the beginning and end of the working day, zero checks received when checking the operation of the printing mechanism) must be submitted along with the cash register report.

When working on a cash register, a cash register tape must be used and executed. A cash register tape is a document confirming the amount of cash received.

During the inter-inventory period, they are stored in packaged (folded and sealed) form. Control tapes must be destroyed within 15 days after the last inventory and verification of the product report. In this case, a tax inspector must be invited to prepare a fiscal report.

Cash register tapes are destroyed according to the act. The act must indicate:

Name of the organization;

Composition of the commission;

Readings of cash register counters;

KKM brand, year of manufacture and serial number;

KKM registration number;

Inventory period;

Receipt numbers, counter readings at the beginning and end of the tape;

Amount of revenue per tape;

Confirmation that the revenue is recorded in the cashier-operator's journal and capitalized in the organization's cash book.

At the end of the act they write: “During a random check of the compliance of data from cash register tapes, cash reports, the cashier-operator’s journal, the organization’s cash book and the removal of a fiscal report using the tax inspector’s password for the specified period, no discrepancies were found.”

The act is drawn up in two copies: one for the tax office, the other for a small enterprise.

The withdrawal of a fiscal report using the tax inspector’s password is formalized by the Act on the transfer of the readings of summing cash counters to zeros and the registration of control counters of the cash register (form No. KM-1). This act is attached to the act for the destruction of cash register tapes.

For each cash register, the enterprise must create a cashier-operator journal according to the unified form No. KM-4.

The journal is used to record transactions regarding the receipt and expenditure of cash (revenue) for each cash register of the enterprise, and is also a control and registration document of meter readings.

The journal must be numbered, laced, sealed with the seal of the enterprise and signed by the manager, chief accountant and tax inspector.

Entries in the journal are kept by the cashier-operator daily in chronological order in ink or a ballpoint pen. Blots in the journal are not allowed. All corrections must be agreed upon and certified by the signatures of the cashier-operator, manager and chief accountant of the organization.

The following indicators are recorded in the columns of the cashier-operator’s journal:

Date – day, month, year;

Last name, first name, patronymic of the cashier-operator;

Counter number;

Indications of the control counter that registers the transfer of summing money counters - meter readings in the “Z” mode, which increases by one when transferring summing money counters to zero;

Readings of summing money counters at the beginning of the working day (shift);

Signatures of the cashier and administrator confirming the readings of cash counters at the beginning of the working day (shift);

Readings of summing cash counters at the end of the working day (shift);

Signatures of the cashier and administrator confirming the readings of cash counters at the end of the working day (shift);

The amount of revenue for the day according to the readings of summing cash counters;

The amount of cash deposited at the organization's cash desk;

The amount of revenue from paid documents (when the buyer pays for goods by checks and other means of payment);

Total revenue;

Cash balance at the end of the day in the cash register;

The amount of shortages (surpluses) identified as a result of the inspection;

The amount of money returned to customers for unused checks in the event of a return of goods or a check mistakenly punched by the cashier-operator. In confirmation of this fact, an act on the return of money to buyers (clients) for unused cash receipts, drawn up in Form No. KM-3, is attached to the cashier-operator’s report;

Signatures at the end of the cashier's working day.

If the enterprise operates without a cashier-operator, that is, the seller accepts revenue from customers, then a journal is kept for recording the readings of the summing cash and control counters of cash register machines operating without a cashier-operator in Form No. KM-5.

The acceptance and delivery of money is recorded in the journal with the joint signatures of the head of the enterprise and a specialist working at the cash register machine. If there is a discrepancy between the results of the amounts on the control tape and the actual revenue, the reasons for the discrepancy are clarified, and the identified shortages or surpluses are entered in the appropriate columns of the journal.

At the end of the working day, a summary report is compiled on the readings of cash register counters and the organization’s revenue for the current working day. This report is compiled according to the unified form No. KM-7 (Information on meter readings of cash register machines and the organization’s revenue). The report is an appendix to the cashier-operator's certificate (form No. KM-6).

The senior cashier draws up a report (information) in form No. KM-7 daily and together with acts, certificates of form No. KM-6, cash receipts and expenditure orders.

In the form, based on the meter readings at the beginning and end of work, revenue is calculated for each cash register; the total revenue of the organization is reduced by the amount of money issued to customers based on their returned checks. This amount is included in the information in accordance with the acts of form No. KM-3. The information is signed by the head and cashier of the organization.

The legislation provides for the introduction of cash register equipment with a new operating principle. Brief information about using online cash register:

- When using a cash register for receiving and issuing cash, information about punched checks is accumulated and transmitted.

- Information collection, control, transmission, accumulation is carried out by the OFD operator.

- Data exchange with the operator is carried out through the SIM card of the cellular operator, the Internet system.

- The transition to new-style cash register equipment is being carried out in stages. The first to switch to the use of cash desks of a new type of enterprise are those that take into account revenue to determine the tax base. The final transition will be completed by July 2018.

During the transition period, it is possible to use both types of cash registers, which are permitted depending on the category of enterprise. Regardless of the type, the cash register must be registered with the cash register department of the territorial branch of the Federal Tax Service. Registration of online cash registers and equipment of the old principle of operation with EKLZ has differences.

Equipment with ECLZ must be registered with the central control center for maintenance. Online cash registers must have an agreement with the OFD operator. Certified organizations, a list of which is posted on the official website of the Federal Tax Service, have the right to carry out information processing operations.

Actions of the enterprise before registering cash register equipment with EKLZ

Cash register equipment of any type is not used without mandatory registration. Equipment and fiscal memory are subject to registration and are replaced annually. In the absence of timely registration of the fiscal memory medium, the cash register is considered unregistered. The use of equipment that does not meet the requirements is equivalent to conducting cash transactions without a cash register, which entails the imposition of significant fines.

Registration of cash register equipment with EKLZ during registration

The procedure is carried out using the same type of operations for any type of cash register that does not belong to online types. Each unit of cash register equipment must receive a registration certificate. Until this point, cash register equipment cannot be used. When using an unregistered cash register, an enterprise expects to be fined.

Before registering cash registers with EKLZ, it is necessary to conclude an agreement with the central service center for the maintenance of equipment. CTO specialists carry out actions to prepare cash registers for registration:

- Draw up a maintenance contract.

- They give you a holographic sticker that acts as a seal for the equipment. After registration, a certificate of sealing of the equipment is provided.

- Information about the enterprise is entered into the cash register data - name, tax identification number, checkpoint.

- Install and activate fiscal memory.

- Enter an initial amount of 1 ruble 11 kopecks to carry out trial operations to check the operation of cash register equipment.

- The first Z-report is taken at the cash register.

- An ECLZ report is taken for the first trial amount.

The trial amount is subsequently entered into the accounting journal, but is not included in the amount of revenue.

Submission of documents to the Federal Tax Service

After completing the registration procedure at the Central Service Center, the organization or individual entrepreneur must submit a package of documents to the Federal Tax Service.

| Document groups | Detailed list |

| Statement | The document is drawn up according to the established form |

| Constituent and general documents of the enterprise | Originals and copies of the OGRN certificate (account sheet), TIN, document on ownership or lease of the premises in which the cash register will be located |

| Documents provided by the CTO | Service agreement, commissioning certificate, technician call log, numbered and stitched in the prescribed manner, sealing stamps, holographic service center stamp |

| Documents accompanying KKM | Invoice for the purchase of equipment, KKM technical passport filled out by a CTO specialist, KKM passport and an additional sheet to it, EKLZ passport |

| Documents for working with equipment | An order for the appointment of a cashier, a journal of a cashier-operator, numbered, filled out, stitched and certified by the head of the enterprise or individual entrepreneur |

| Forms for representative of interests | Power of attorney (the document is not required for a manager or individual entrepreneur who has the right to represent interests without a power of attorney), passport, organization seal |

Along with the general list of documents, the cash register accounting department of the territorial body of the Federal Tax Service may request the submission of additional documents.

Procedure for registering cash register machines with EKLZ

To register cash register equipment with EKLZ, a certain procedure is followed.

| Sequence of actions | Explanation |

| Submission of documents for registration | Submission is carried out to the cash register department of the Federal Tax Service department |

| Acceptance of documents | The inspector determines the time for fiscalization |

| Carrying out fiscalization | After checking the documents in the cash register department of the territorial body of the Federal Tax Service, fiscalization is carried out in the presence of a representative and specialist of the central service center |

| Registration | Registration is carried out within 5 days |

| Issuance of finished documents | The applicant receives a cash register card and originals provided by the company |

Registration of new-style cash registers

The procedure adopted for registering cash registers applies only to old-style equipment, the recording of information of which is provided by EKLZ. When registering online cash registers, they take into account the conditions for the appearance of an additional link in the chain of information transfer - the OFD operator:

- In connection with the introduction of online cash registers, the package of documents was supplemented by an agreement with the OFD operator. According to the new procedure, modernized equipment converted for online cash registers is also registered.

- OFD operator is an organization that receives, processes and stores information about all operations performed on cash register equipment.

- Information from the OFD operator is sent to the Federal Tax Service for further control of cash flow.

For cash register equipment modernized for online cash registers, the procedure corresponds to the registration of new equipment. Registration of modified equipment is preceded by its deregistration. The online cash register is not presented to the tax authority. From February 1, 2017, organizations or individual entrepreneurs can register cash register equipment online through the taxpayer’s personal account. At the same time, the right to register during a personal visit to the Federal Tax Service is retained. To submit applications on paper, new forms were introduced by order of the Federal Tax Service of the Russian Federation dated May 29, 2017 No. ММВ-7-20/484@.

Registration online KKM through your personal account

Setting up cash registers with an online system for transmitting information through the taxpayer’s personal account requires prior registration on the official website of the Federal Tax Service. The portal contains detailed instructions on the procedure. To gain access and carry out the procedure, you must issue a qualified digital signature. After gaining access, you can register the equipment.

| Procedure | Description |

| Login to your personal account and the “KKT” tab | You must use the “Register cash register” function |

| Water addresses | Indicate the address of the location where the cash register equipment will be located and the name of the point or office |

| Data on cash register equipment | Enter data about the model, serial number, the brand is indicated based on the data in the drop-down list. The absence of a type of equipment in the list indicates a non-compliance of the CCP with the requirements |

| Fiscal storage number | Indicate the data available in the KKM passport |

| Cash register application mode | When using the equipment in normal mode, no additional information is provided |

| Data about the OFD operator | You need to use the list of operators officially registered with the Federal Tax Service |

After completing data entry, the document must be signed and sent. Based on the results of the request, the Federal Tax Service must send the number assigned to the cash register. The number must be entered into the equipment data, the receipt must be printed and the final action must be taken – “complete registration”. In your personal account, a record is made from a printed receipt about the time of registration, fiscal document numbers and attribute.

Registration with the OFD operator

Cash register equipment must be registered with the OFD operator. You will need to go to the website of the selected OFD operator and record the information:

- The number assigned by the Federal Tax Service during registration.

- Cash register type - equipment model.

- Data of cash register equipment specified in the passport - serial number.

- Fiscal storage numbers.

After registration, the owner of the equipment selects a tariff, on the basis of which an electronic invoice is generated. Work with cash register equipment will be available after payment has been made.

When registering cash register equipment, businesses may make mistakes. Enterprises must take into account the conditions of the new procedure for registering online cash registers:

- Registration does not require an agreement with the central service center.

- The Federal Tax Service cannot require the presentation of a certified journal of the cashier-operator due to the lack of need to use them.

When operating the equipment, daily cashier reports are saved; the log can only be used for internal needs (Read also the article: → “

We recommend reading

Degas E. “Blue Dancers. Essay based on the painting by Edgar Degas “Blue Dancers Dancers in Blue”

Degas E. “Blue Dancers. Essay based on the painting by Edgar Degas “Blue Dancers Dancers in Blue” We reflect in the RSV reimbursement of social insurance expenses for the last year Appendix 2 line 090 of the calculation of insurance premiums

We reflect in the RSV reimbursement of social insurance expenses for the last year Appendix 2 line 090 of the calculation of insurance premiums Olesya Malibu: Russian clone of Pamela Anderson

Olesya Malibu: Russian clone of Pamela Anderson The problem of human spirituality

The problem of human spirituality