Cash flows in the form of income taxes are significant payments that fill the federal and regional budgets. The tax period for income tax is significant - a calendar year. But the state is not willing to wait that long to get its share of the pie. Therefore, during the year the legislator provided for the payment of advance tax payments. And it is easier for an organization to pay taxes in installments.

Calculating advance payments based on profits seems simple at first glance. But, firstly, you need to reasonably select the appropriate calculation option, fixing it in the accounting policy (quarterly or based on actual profit). Secondly, the quarterly calculation has its own subtleties with advance payments, which sometimes confuse the accountant. Let's look at this in detail in two approaches. In this article we will discuss the calculation rules. Using specific examples, we will make calculations and enter the required amounts into the declaration.

1. Who pays advances on profits

2. Types of advance payments

3. Calculation of advance payments based on quarterly profits

4. Monthly advances on profits based on estimated profits for the previous quarter

5. Examples of calculating advance payments by quarter

6. Subtleties of calculating advance payments

7. Monthly advances on profits based on actual profits

8. Advance payments in the income statement

9. Deadlines for payment of advances on profits

So, let's go in order.

1. Who pays advances on profits

Almost all income tax payers pay advances on profits. In this case, neither the size nor the nature of the company’s activities, nor the calculated amount of tax matters.

The list of those who do not pay advance income tax payments is not long. Such organizations are directly listed in the Tax Code of the Russian Federation. These are budgetary institutions such as libraries, concert organizations, museums, and theaters.

2. Types of advance payments

There are 3 types of advances on profits (Article 286 of the Tax Code), which can be roughly called:

- Quarterly payments

- Monthly payments based on estimated profit,

- Monthly payments calculated based on the actual profit received by the organization for the month.

Data on the frequency of advance payments and submission of declarations are given in Table 1.

Table 1

3. Calculation of advance payments based on quarterly profits

Typically, calculating advance payments based on quarterly profits (quarterly advance payments) does not cause any difficulties for an accountant. You just need to know the basic rules:

- Organizations that have the right to pay only quarterly advance payments have revenue for the previous 4 quarters did not exceed an average of 15 million rubles per quarter without VAT. For newly created organizations, sales revenue should not exceed 5 million rubles per month or 15 million rubles per quarter (Example 1).

- The right to pay only quarterly advance payments is also from some other legal entities listed in paragraph 3 of Article 286 of the Tax Code of the Russian Federation - budgetary and autonomous institutions, non-profit organizations that do not have income from the sale of goods (works, services), participants in simple partnerships and some others.

- Advances on profit for the quarter are considered based on the tax base for the reporting period. The amount payable is obtained as the difference between the calculated advance for the reporting period and the advance determined for the previous reporting period (Example 4).

Example 1

It is necessary to determine whether the company has the right to make quarterly payments if the revenue excluding VAT is:

1st quarter of 2017 - 25 million rubles,

2nd quarter 2017 - 8.5 million rubles,

3rd quarter of 2017 - 9.5 million rubles,

4th quarter of 2017 - 29 million rubles,

The average revenue for 4 quarters is checked.

Average revenue for 4 quarters = (25 + 8.5 + 9.5 + 29) / 4 = 18.0 million rubles.

Conclusion - from the 1st quarter of 2018, the organization is obliged to pay monthly income tax payments.

4. Monthly advances on profits based on estimated profits for the previous quarter

The rules for calculating monthly advance payments for each quarter are given in paragraph 2 of Article 286 of the Tax Code of the Russian Federation.

For ease of understanding, we will use calculation formulas, conventionally denoting:

- AMn – monthly advance payment for the nth quarter,

- АКn – quarterly advance payment for the nth quarter,

- n – quarter number from 1 to 4.

Formulas for calculating advance payments of profit by quarter:

- Monthly advance payment in 1st quarter

AM1 = AM4, where AM4 is the monthly payment of the 4th quarter of the previous year,

- Monthly advance payment in 2nd quarter

AM2 = AK1 / 3,

- Monthly advance payment in 3 quarter

AM3 = (AK2 - AK1) / 3,

- Monthly advance payment in 4th quarter

AM4 = (AK3 - AK2) / 3.

When preparing a declaration for the reporting period, the actual data obtained for the period are analyzed. If the calculated advance payment for the current quarter is greater than the total quarterly and monthly payments paid, then an additional payment of the quarterly advance payment is required in the amount of the difference.

5. Examples of calculating advance payments by quarter

Example 2

According to the declaration for the half-year, monthly advance payments due in the 3rd quarter amounted to 10 thousand rubles. per month. According to the declaration for 9 months, the calculated advance payment is 55 thousand rubles, quarterly payments for the last quarter are 10 thousand rubles. Calculate the quarterly surcharge taking into account the monthly advance payments paid.

- - 10 - 3 * 10 = 15 thousand rubles.

If suddenly the amounts of advances paid turn out to be more than those calculated for the reporting period, then advance payments based on the results of the reporting period are counted against the tax payment based on the results of the next reporting (tax) period (clause 1 of Article 287 of the Tax Code of the Russian Federation).

But the Declaration indicates the estimated data for monthly advance payments for the next period.

Example 3

According to the declaration for the half-year, monthly advance payments due in the 3rd quarter amounted to 20 thousand rubles. per month. According to the declaration for 9 months, the advance payment is 50 thousand rubles, quarterly payments for the last quarter are 10 thousand rubles. Determine what data needs to be reflected in the Declaration for 9 months.

- – 10 – 3 * 20 = – 20 thousand rubles. - there was an overpayment.

Such overpayment is reflected in lines 280,281 of Sheet 02 of the Declaration. The overpayment can be offset against the tax payment based on the results of the next reporting (tax) period (clause 1 of Article 287 of the Tax Code of the Russian Federation).

6. Subtleties of calculating advance payments

1. Only in the declaration for 9 months the amounts of advance payments for the 4th quarter of the current and 1st quarter of the next year are determined (lines 320, 330, 340 of Sheet 02 of the Declaration).

If, when preparing a declaration for 9 months, the limit is 15 million rubles. has not been exceeded, planned monthly payments are not reflected in the declaration.

But if suddenly (as in our example) based on the results of the declaration for the year, the specified limit is exceeded, then in the opinion of the regulatory authorities, planned monthly advance payments should be reflected in the declaration for 9 months (Letter of the Ministry of Finance of the Russian Federation dated December 24, 2012 N 03-03-06/ 1/716).

From the text of the letter we can conclude that you will need to submit an updated declaration within 9 months. Otherwise, the Federal Tax Service simply has nowhere to find out the amount of monthly advance payments that the organization will need to pay in the 1st quarter.

There is another point of view - do not submit an updated declaration for 9 months, reflect the monthly advance payments of the 1st quarter only in the declaration for the year. But then we will violate the provisions of clause 5.11 of the Order of the Federal Tax Service of Russia dated October 19, 2016 N ММВ-7-3/572@, which determines the procedure for filling out the declaration. After all, it clearly states that lines 290-310 in the declaration for the tax period are not filled out.

2. When keeping records in the 1C program it is necessary to reflect in the settings the fact of the transition to paying monthly advance payments (Main - Tax and reporting settings - Income tax - Procedure for paying advance payments - select “Monthly according to estimated profit”).

3. The calculation of lines 210 (220 and 230) includes both quarterly (lines 180 (190, 200)) and monthly (lines 290 (300, 310)) advance payments reflected in the declaration for the previous reporting period.

For an example of calculating monthly payments, see the video.

7. Monthly advances on profits based on actual profits

In this case, it is necessary to submit a notification to the Federal Tax Service about the transition to monthly advance payments based on actual profits. The notification is submitted for the next year no later than December 31 of the current year.

With this method, the Declaration is submitted monthly, the advance is calculated based on the actual profit for the month.

In the event of a transition to paying monthly advance payments based on the actual profit received, the reporting periods will be one month, two months, three months, and so on until the end of the calendar year (Clause 2 of Article 285 of the Tax Code of the Russian Federation).

Calculation of advance payments on profit can be done using the formula:

AM of the reporting period = Tax base of the reporting period x Tax rate.

Each time at the end of the reporting period, the amount to be paid is determined:

AM for additional payment = AM reporting - AM previous.

8. Advance payments in the income statement

Advance payments in the income statement are reflected in the lines:

- 180 (190, 200) – advance payments for the periods 1st quarter, half year, 9 months,

- 210 (220, 230) – advance payments reflected in lines 180 (190, 200) for the previous reporting period,

- 270, 271 (280, 281) – advances for additional payment (reduction) for the reporting period,

- 290 (300, 310) – monthly advance payments that must be paid in the months following the reporting period,

- 320 (330.340) – monthly advance payments due in the 1st quarter of the next year (these lines are filled in only in the declaration for 9 months).

The main thing to remember when filling out the declaration is that advance payments are reflected as accrued, and not as actually paid. Payment of advance payments on profits is not reflected in the declaration. Filling out the declaration.

9. Deadlines for payment of advances on profits

Payment of advance payments on profits must be made within the time limits established by Article 287 of the Tax Code of the Russian Federation:

- Quarterly advance payments paid no later than the deadline established for filing tax returns for the corresponding reporting period - April 28, July 28, October 28. If the deadline falls on a weekend or holiday, payment is made on the first business day after the weekend or holiday.

- Deadlines for payment of advances on profits for organizations paying monthly advance payments during the reporting period - no later than the 28th day of each month of this reporting period.

- Deadlines for payment of advances on profits for organizations paying monthly advance payments based on the actual profit received, - no later than the 28th day of the month following the month based on the results of which the tax is calculated.

Read and study examples of calculations and filling out advances in the declaration. And if you already have questions on the topic, ask in the comments!

Calculation of advance payments based on profit - general rules

One of the largest tax collections in Russia is the profit tax. Its payers are organizations, both Russian and foreign, operating in the country. However, the tax is not paid in a lump sum - advances on the income tax must be paid throughout the tax period. The frequency of their transfer depends on which category the payer belongs to. Today we will tell you how income tax advances are calculated and paid, as well as who pays them.

Article No. 25 of the country's Tax Code describes the rules by which company profits are subject to duty. The object of taxation is profit, as is already clear from the name of the tax itself. In fact, the fee is paid on the difference between income and expenses. Profit tax is considered direct, since its size depends entirely on the company’s labor efficiency, calculated in monetary terms.

Tax payers are all legal entities in Russia: limited liability companies, closed and open joint-stock companies, etc. It is important that the company operates on the traditional tax system – OCHO. Accordingly, companies using special regimes (STS, Unified Agricultural Tax and others) are exempt from tax. Gambling business owners and Skolkovo residents also do not pay the profit tax. Secondly, payers are foreign companies whose income is accumulated in Russia. Their list includes companies that have permanent representative offices in the country, are managed from Russia or have signed an international tax treaty and are therefore tax residents in the country.

Firms that receive income in cash or in kind pay income tax. Profit also includes other non-operating income received from bank deposits, money collected for rent or sublease, and the like. Taxable profits are accounted for without excise taxes and VAT.

How to pay profit tax?

All year long, companies pay advance payments on a lucrative fee. Their frequency depends on what order the organization has chosen and what its level of income is. The procedure for paying advances is directly related to the amount of profit received by the company for the four quarters preceding the reporting period. Regarding companies whose revenue does not exceed sixty million Russian rubles per year, they make advances quarterly.

We will tell you in detail who the payer is, how to pay income tax, consider special conditions for payment and answer questions that may arise from a person delving into the stated topic.

Companies receiving greater income have the right to:

- pay quarterly tax or monthly preliminary payments during the quarter;

- make advances based on actual profits, “in hand”, submitting declarations on a monthly basis.

The payment scheme is chosen once a year and is fixed in the company’s tax accounting policy. When changing the scheme, you must notify the tax inspector in advance.

Let's take a closer look at who should pay advances and with what frequency. Quarterly, excluding monthly payments, this can be done by:

- Companies with annual revenues of less than 60 million rubles.

- Foreign companies with official permanent representative offices.

- Autonomous institutions.

- Investors of goods and production sharing agreements.

- Companies that do not have cash income from commercial activities.

- Budgetary enterprises, excluding theaters, libraries and museums.

- Firms that have signed papers on joint activities.

- Companies that have transferred their property to trust management.

Advances are paid monthly with a quarterly surcharge by firms that were able to earn more than 60 million rubles in the four quarters preceding the reporting period. Every month, based on the money actually earned, all organizations can transfer advance contributions at their own request, voluntarily.

There are several advance payment schemes

Advances of profitable collection: we calculate

If we talk about monthly advances, you can pay them in two ways:

Based on actual profit.

By choosing this method, the company immediately calculates the profit received for the month. The advance payment for the previous month is paid before the 28th day of the current month. Let's look at an example.

Unicorn LLC transfers advances once a month, based on the profit received. During the month of May, the company earned two hundred thousand rubles. When this figure is multiplied by the base rate for profitable collection - 20%, it turns out that by June 28, Unicorn LLC must deposit forty thousand rubles into the state treasury. If the next month's profit is different, the advance amount will also change.

“Looking back” at the tax for the past quarter.

In this case, advances are paid in advance - before the 28th of the tax month. Simply put, for July the advance payment must be made before July 28th.

Table 1. Amounts of monthly advances

When the quarterly period ends, the organization calculates the tax amount calculated from the actual revenue and the figure indicating the monthly advance. If the first figure is higher, you will have to pay extra at the end of the quarter. If the second digit is higher, the company will have an overpayment, which can be used for further payments.

We will tell you more about advance payments in How to calculate them correctly, and also give examples and instructions.

Let's look at an example. Dragon LLC transfers advances based on the results of previous quarters. In six months the company earned 800 thousand rubles, in the first quarter - 200 thousand. Profit for the second quarter will be equal to 600 thousand rubles (800-200), tax at a twenty percent rate will be 120 thousand rubles. Thus, every month of the third quarter, Dragon LLC will deduct 40 thousand rubles (we divide the tax amount by three months).

Video - Calculation of advance payments for income tax

How do newly created companies pay?

If the company has just started its activities, it can also choose an advance payment scheme from the two above. If a company wants to pay monthly after the fact, then the tax service must be notified about this. Thus, a company created in December will make the first payment for December and January profits - no later than February 28. Further, the declaration must be submitted monthly.

If the payment scheme is based on payments in previous quarters, notification to the inspectorate will not be required. The first advance payment for a company that began operating in December will be calculated for profits from December to March. From the sixth quarter of work, the procedure for calculating advances becomes general, as we described above. Since 2016, it has been legislated that newly founded companies whose quarterly profit does not exceed 15 million Russian rubles, and whose monthly profit is no more than five million, can pay advances quarterly.

Let's sum it up

All firms operating under OCHO are required to pay advances on profit levy. Payments are calculated in three ways - monthly based on actual profits, quarterly or every month with an additional payment for the quarter. Each method has its own nuances, which we described in detail.

Corporate income tax is one of three taxes and is paid exclusively by organizations, regardless of their legal form (LLC, JSC, etc.). An analogue of income tax for individual entrepreneurs is personal income tax.

Income tax is a direct tax and is calculated based on the income received by the organization, reduced by expenses incurred during the reporting period.

When calculating tax, an organization must first determine what expenses and income must be taken into account in the reporting (tax) period for which the advance payment or tax will be calculated. The date of recognition of income and expenses is determined by one of the methods selected by the organization in advance and enshrined in the accounting policy.

Methods for recognizing income and expenses

In total, there are two methods for determining the date of receipt of income and expenses: the accrual method and the cash method. Let's take a closer look at them.

Cash method

Organizations using the cash method take into account income and expenses on the date of actual payment.

Income is taken into account on the date of receipt of funds into the account, into the cash register, at the time of receipt of property and property rights, and on the date of payment of debt.

Expenses are taken into account on the date of their actual payment, taking into account the following features:

- Costs for salary, material costs and interest payments for the use of borrowed funds are taken into account on the date of debiting funds from the organization’s account or payment from the cash register.

- Expenses for the purchase of raw materials and materials are taken into account as they are written off for production.

- Expenses for paying taxes, fees and other obligatory payments are taken into account on the date of their actual payment.

Who has the right to use the cash method?

This method of accounting for income and expenses can only be used by those organizations whose income for the last 4 quarters did not exceed 1 million rubles. per quarter (total no more than 4 million rubles for 4 quarters).

Who cannot use the cash method

You may not use the cash method:

Credit consumer cooperatives.

Microfinance organizations.

Participants in simple partnership and trust property management agreements.

Accrual method

Unlike the cash method, when using the accrual method, the date of actual receipt of funds into the account (the date of expenses) does not matter. Income and expenses are recorded in the period in which they were incurred.

Income is taken into account on the date of concluding an agreement or other document justifying its occurrence, taking into account the features established by Art. 271 Tax Code of the Russian Federation.

Expenses are recorded in the period in which they arise based on the terms of the transaction. For material expenses, the recognition date is the date of transfer of raw materials and materials into production or the date of signing the acceptance and transfer certificate of services (work) for production services.

Non-operating and other expenses are taken into account on the date of settlement in accordance with the terms of the concluded agreement or on the date of presentation of documents.

More details on the procedure for accounting for expenses when using the accrual method can be found in Art. 272 Tax Code of the Russian Federation.

Please note that the accounting method you choose applies to both income and expenses. It is impossible to choose one method for accounting for income and the other for expenses. You can change the selected method once a year by notifying the tax authority in advance.

Income and expenses

Income

When calculating income tax, income is divided into sales and non-sales. Sales income includes proceeds from the sale of goods, works or services, as well as property rights. Non-operating income – all other income listed in Art. 249 Tax Code of the Russian Federation.

Note: income not taken into account when calculating income tax is listed in Art. 251 Tax Code of the Russian Federation. This list is closed and is not subject to broad interpretation.

Expenses

Expenses are also divided into operating and non-operating. Sales costs can be direct (accounted for as the goods are sold in the cost of which they were taken into account) and indirect (accounted for during the period of their implementation).

Direct sales costs include material costs, depreciation costs and wages of employees involved in the sales process.

Note: expenses taken into account when calculating income tax must be documented, justified and aimed at generating income. If at least one of the specified conditions is not met, recognition of the organization’s expenses will be denied. This often happens when the tax authority recognizes the organization’s counterparty as unscrupulous, the expenses unreasonable, or the transaction imaginary.

Tax and advance payments for income tax

The tax is paid once at the end of the year.

The frequency of advance payments depends on the method chosen by the organization. There are three ways to pay advances on income tax:

- Monthly payments based on actual profits.

- Quarterly advances with monthly payments.

- Quarterly advances without paying monthly payments.

Let's take a closer look at each of the methods.

Monthly advances

The procedure for making advance payments monthly based on actual profits is the most common and is used by the vast majority of organizations.

There are no special conditions or restrictions for its use. Advance payments based on actual profits are paid at the end of each month. In total, during the year, the organization must pay 11 advance payments and tax at the end of the year, and also submit 12 tax returns to the Federal Tax Service (for each month).

Monthly advances are calculated using the following formula:

(Income – Expense x Tax rate) – Advance calculated for the previous month

Note: income and expenses are taken into account on an accrual basis from the beginning of the year.

An example of calculating advances based on actual profits

Data for calculating advance payment for January:

Income for January – 200,000 rubles.

Expense for January – 75,000 rubles.

Tax rate – 20%

Monthly advance for January:

(200,000 – 75,000) x 20% = 25,000 rub.

Data for calculating the advance for February:

Income for January-February – 320,000 rubles.

Expense for January-February – 170,000 rubles.

Monthly advance for January

(320,000 – 170,000) x 20%) – 25,000 = 5,000 rubles.

The advance payment for the remaining reporting periods is calculated in a similar manner.

Quarterly advances without payment of advance payments

Organizations whose income for the last 4 quarters did not exceed 15 million rubles can pay advances based on quarterly results (3 times a year). per quarter.

This method cannot be used:

- Theaters;

- Museums;

- Libraries;

- Concert organizations.

Note: Newly created organizations pay quarterly advances (no monthly payments) until a full quarter has passed from the date of their registration. If after the quarter the company’s revenue does not exceed 1 million rubles. per month and 3 million rubles. per quarter, she can continue to pay quarterly advances. In case of excess, she is obliged to switch to paying monthly advance payments from the next quarter.

An example of calculating quarterly advances without paying monthly payments

Data for calculating the advance 1st quarter:

Income for 1 quarter – 1,200,000 rub.

Consumption per 1 sq. – 550,000 rub.

Tax rate – 20%

Trade fee - not paid

Advance calculated for the 1st quarter

(Income – Expense x Tax Rate)

(1,200,000 – 550,000) x 20% = 130,000 rub.

Advance payment to the budget

Advance payment to the budget for the 1st quarter = Advance calculated for the 1st quarter

130,000 rub.

Data for calculating the half-year advance:

Income for the six months (cumulative total) – RUB 3,200,000.

Expenses for the half-year – RUB 1,450,000.

Advance calculated for half a year

(3,200,000 – 1,450,000) x 20% = 350,000 rub.

Advance payable for half a year

Advance calculated for half a year – Advance calculated for 1st quarter

350,000 – 130,000 = 220,000 rubles.

Data for calculating advance payment for 9 months:

Income for 9 months – 5,000,000 rubles.

Expense – RUB 3,200,000.

Advance calculated for 9 months

(Income – Expense) x Tax rate

(5,000,000 – 3,200,000) x 20% = 360,000 rub.

This article will be useful to those taxpayers who make quarterly payments based on the results of the quarter plus monthly advance payments.

The article will help:

- calculate advance payments for income tax for the first half of the year,

- find out about the timing of advance payments based on the results of the first half of the year,

- fill in the appropriate sections and lines in the declaration.

Example

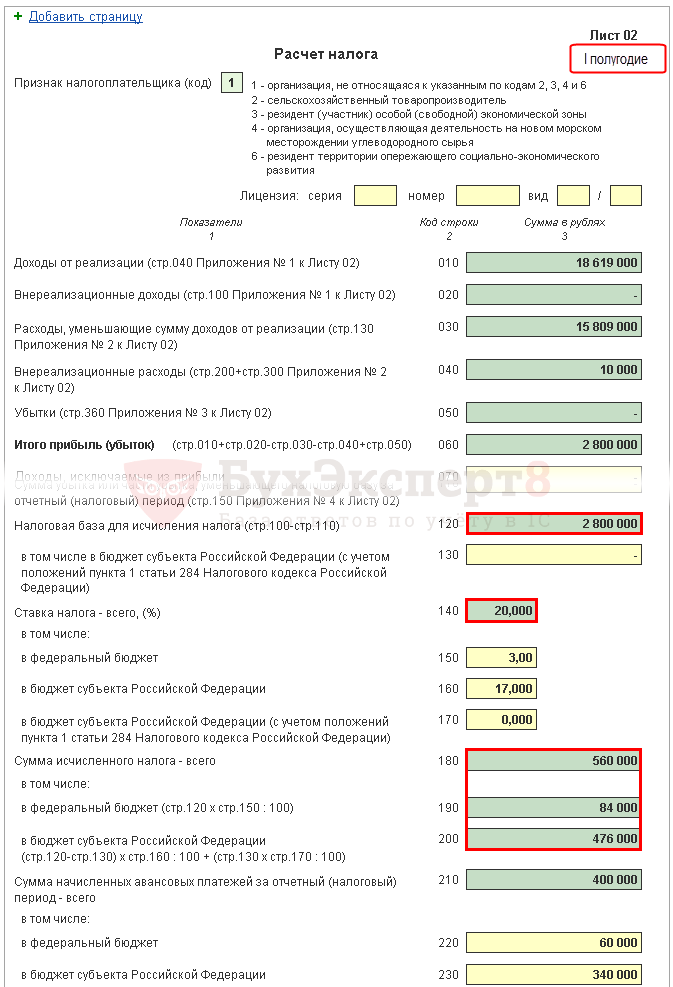

Sheet 02 Calculation of income tax and advance payments

Let's look at the step-by-step filling out of the Sheet 02 declaration regarding the calculation of income tax for the first half of the year and the amount of monthly advance payments for the third quarter.

Step 1. Determine the amount of income tax for the first half of the year (pages 180-200)

The amount of income tax in 1C is calculated automatically based on the tax base indicated on page 120 and the rate on page 140 (150-170).

Check the calculation for the first half of the year using the formula:

In our example, the total amount of income tax (page 180) is 2,800,000 x 20% = 560,000 rubles, including:

- to the federal budget (p. 190) - 2,800,000 x 3% = 84,000 rubles;

- to the budget of a constituent entity of the Russian Federation (page 200) - 2,800,000 x 17% = 476,000 rubles.

Step 2. Enter the amount of advance payments calculated for the previous period (pages 210-230)

Advance payments that the organization must pay for the period of the first half of the year must be indicated on page 210 (220, 230) in 1C manually, since they are calculated according to the declaration for the first quarter of the current year and consist of:

- tax calculated based on the results of the first quarter (pages 180, 190, 200);

- accrued advance payments payable in the second quarter (lines 290, 300, 310);

- trade tax paid in the first quarter, by which the profit tax for the first quarter was reduced (p. 267).

In lines 220, 230 in the declaration for the first half of the year, manually enter the amounts calculated using the formula:

In our example, the amount of accrued advance payments for the first half of the year is:

- federal budget (p. 220) - 30,000 rubles. + 30,000 rub. = 60,000 rub.;

- budget of a constituent entity of the Russian Federation (p. 230) - 170,000 rubles. + 170,000 – 30,000 rub. = 310,000 rub.

Step 3: Check the amount of trade fee paid (pages 265, 266, 267)

Lines 265, 266, 267 of Sheet 02 of the declaration will be filled out automatically in 1C if the organization has registered a retail outlet in the program and automatically calculates the trade fee.

In the declaration for the first half of the year, these lines are filled in as follows:

- p. 265 – the amount of trade tax actually paid to the budget of the constituent entity of the Russian Federation since the beginning of the year. In our example, the amount is 60,000 rubles.

- line 266 – the amount of the trading fee by which the profit tax was reduced in previous reporting periods of the current year. This line should be equal to the amount on page 267 in the declaration for the first quarter.

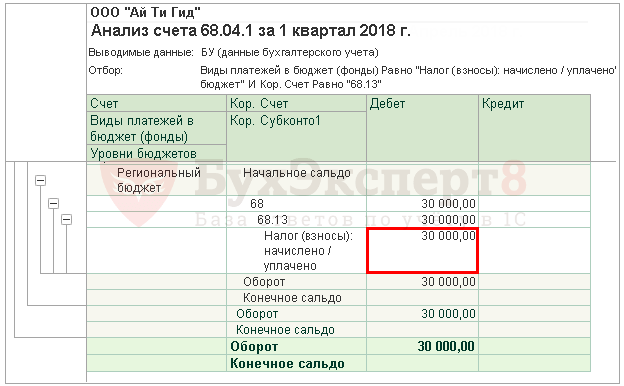

In 1C, in the half-year declaration, line 266 automatically fills in the amount of the reduction in income tax on the trading fee for the first quarter, i.e. this is the turnover:

- Dt 68.04.1 ( Budget level - Regional budget, Type of payment - Tax accrued/paid).

- Kt 68.13 ( Type of payment - Tax accrued/paid).

In our example, page 266 is equal to 30,000 rubles.

- p. 267 – the amount of the trade fee, which reduces the calculated income tax for the first half of the year to the republican budget. The line indicator cannot be greater than the amount on page 200 “Amount of accrued tax to the budget of a constituent entity of the Russian Federation.”

In 1C, line 267 automatically fills in the amount of the reduction in income tax on the trading fee for the first half of the year, i.e. this is the turnover:

- Dt 68.04.1 ( Budget level - Regional budget, type of payment - Tax accrued/paid).

- Kt 68.13 ( Type of payment - Tax accrued/paid).

In our example, page 267 is equal to 60,000 rubles.

Step 4. Determine the amount of tax to be paid additionally (pages 270, 271) or reduced (pages 280, 281)

Now it is necessary to determine what happened more: the actual amounts of tax calculated based on the results of the first half of the year (pages 190, 200), or the amount of accrued advance payments that the taxpayer was obliged to pay in this period (pages 220, 230) taking into account the trade tax (p. 267), calculated based on the results of the declaration for the first quarter.

Step 4.1. Federal budget

If page 190 is greater than page 220, then the tax to the federal budget for the first half of the year must be paid additionally, i.e. in 1C line 270 will be automatically filled in according to the formula:

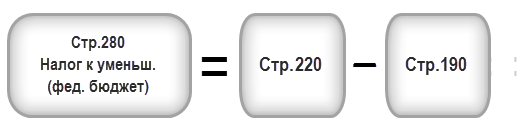

If page 190 is less than page 220, then the tax to the federal budget based on the results of the first half of the year will be reduced, i.e. in 1C line 280 will be automatically filled in according to the formula:

In our example, line 190 (amount of 84,000 rubles) is greater than line 220 (amount of 60,000 rubles), therefore, the tax to the federal budget for the first half of the year will be additionally paid:

- page 270 = 84,000 - 60,000 = 24,000 rub.

Step 4.2. Budget of a constituent entity of the Russian Federation

If page 200 is greater than the sum (page 230 + page 267), then the tax to the budget of the constituent entity of the Russian Federation for the first half of the year must be paid additionally, i.e. in 1C line 271 will be automatically filled in according to the formula:

If page 200 is less than the sum (page 230 + page 267), then the tax to the budget of the constituent entity of the Russian Federation based on the results of the first half of the year will be reduced, i.e. in 1C line 281 will be automatically filled in according to the formula:

In our example, line 200 (amount 476,000 rubles) is greater than the sum of lines 230 and 267 (370,000 = 310,000 + 60,000), therefore, the amount of tax to the budget of a constituent entity of the Russian Federation at the end of the first half of the year will be additionally paid:

- page 271 = 476,000 - 310,000 - 60,000 = 106,000 rubles.

Step 5. Determine the amount of advance payments due in the third quarter (pages 290-310)

Organizations paying monthly advance payments must, based on the results of the first half of the year, calculate the advances payable in the third quarter. Such payments are reflected on line 290 (300, 310).

In 1C, these lines are filled in manually. Advance payments payable must be calculated using the formula:

In our example, the amount of monthly advance payments payable in the third quarter is calculated:

- total (p. 290) - 560,000 rub. – 200,000 rub. = 360,000 rub., incl.:

- to the federal budget (p. 300) = 84,000 rubles. – 30,000 rub. = 54,000 rub.;

- to the budget of a constituent entity of the Russian Federation (p. 310) = 476,000 rubles. – 170,000 rub. = 306,000 rub.

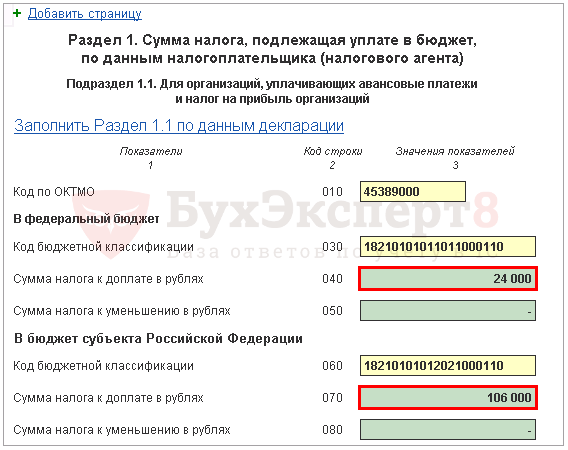

Section 1 Subsection 1.1 Final data on tax payment for the first half of the year

Filling out the final data on additional payment or reduction of income tax in the first half of the year is carried out in 1C automatically according to the following algorithm.

If the tax amount is due for additional payment, i.e., line 270 or line 271 is filled out in Sheet 02, then the amount indicated in them is transferred to Section 1 Subsection 1.1: PDF

- on page 040 - from page 270 of Sheet 02 “to the federal budget”;

- on page 070 - from page 271 of Sheet 02 “to the budget of a constituent entity of the Russian Federation.”

If the tax amount is reduced, i.e. line 280 or line 281 is filled out in Sheet 02, then the amount indicated in them is transferred to Section 1 Subsection 1.1: PDF

- on page 050 - from page 280 of Sheet 02 “to the federal budget”;

- on page 080 - from page 281 of Sheet 02 “to the budget of a constituent entity of the Russian Federation.”

In our example, the amount of income tax for the first half of the year to the federal budget and the budget of the constituent entity of the Russian Federation was subject to additional payment.

Based on this norm, pay the tax for the first half of the year specified in Section 1 of Subsection 1.1. necessary until July 28.

If the deadline for tax payment falls on a weekend or holiday, then the deadline is postponed to the first working day following it (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

In our example, additional payment of income tax must be made before July 30, 2018. (July 28 - day off):

- to the federal budget - 24,000 rubles.

- to a subject of the Russian Federation - 106,000 rubles.

Familiarize yourself with the procedure for paying income tax:

- federal budget;

- budget of a constituent entity of the Russian Federation.

Section 1 Subsection 1.2 Advance payments for the third quarter

Section 1 of Subsection 1.2 of the declaration reflects monthly advance payments that must be paid in the third quarter.

The amount of advance payments for the third quarter was calculated on pages 300, 310 of Sheet 02. It is automatically distributed to Subsection 1.2 in the amount of 1/3 of the quarterly amount:

- pp. 120-140—from p. 300 “to the federal budget”;

- pp. 220-240—from p. 310 “to the budget of a constituent entity of the Russian Federation.”

Based on this norm, in the third quarter it is necessary to pay the advance payments specified in Section 1 of Subsection 1.2:

- until July 28;

- until August 28;

- until September 28.

If the deadline for payment of advance payments falls on a weekend or holiday, then the deadline is postponed to the first working day following it (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

- Payment of income tax to the federal budget;

- Payment of income tax to the budget of a constituent entity of the Russian Federation.

In our example, payment of advance payments in the third quarter should be made:

- until July 30, 2018 (July 28 - day off):

- to a subject of the Russian Federation - 102,000 rubles.

- until August 28, 2018:

- to the federal budget - 18,000 rubles.

- to a subject of the Russian Federation - 102,000 rubles.

- until September 28, 2018:

- to the federal budget - 18,000 rubles.

- to a subject of the Russian Federation - 102,000 rubles.